Kostov Ivan

Ph.D., Chief assistant professor

University of National and World Economy

Sofia, Bulgaria

THE FACTORING MARKET – TRENDS AND PERSPECTIVES

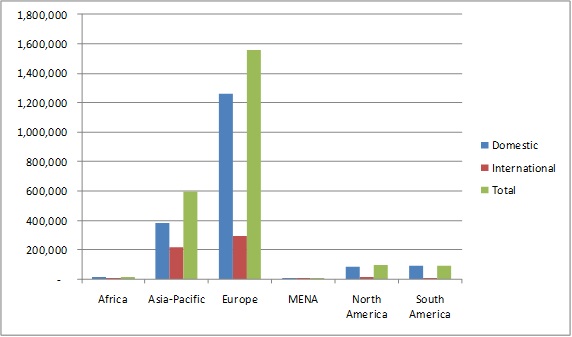

According to Factors Chain International (FCI) in 2015 the global factoring market increases by 1.14% to 2.373 trillion euro. Europe is the largest factoring market with factoring turnover of almost 1.56 trillion euro, which marks a 6% volume increase. (Figure 1).The growth has mainly been driven by domestic factoring turnover and by the source of banking sector which controls approximately 90% of Europe’s factoring turnover.

Figure 1. Factoring turnover by continent in 2015 (in millions euro)

Source: FCI, Own calculations

The second largest global factoring market is in Asia, but it decreased by 8% to 562.99 billion euro in 2015. The North and South America also suffered a decline, down by 6% to 194.17 billion euro.

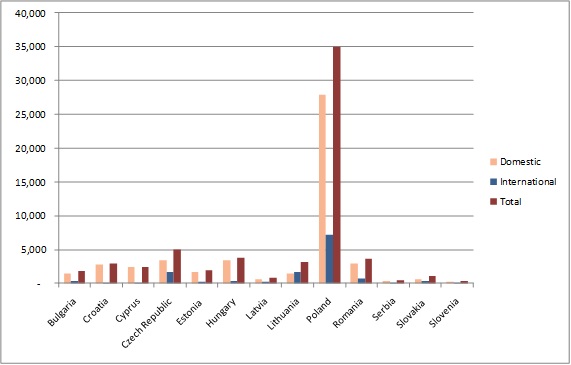

The domestic factoring market is accounted for 1.84 trillion euro (78% of the total market) and the international factoring for 530 billion euro (22%). The top factoring markets in developing countries are Poland, Czech Republic, Hungary, Romania and Croatia.

Figure 2. Factoring turnover in developing countries in 2015 (in millions euro)

Source: FCI, Own calculations

The factoring turnover in Bulgaria in 2015 is about 1.8 billion euro (with 12% increase) and the country is ranked with Cyprus, Estonia and Lithuania according to this indicator. The market of factoring services in Bulgaria has grown 6 times since 2007. There are no official statistical data on national level but based on The International Factors Group (IFG, 2013) there are eight companies providing factoring services on the local market out of which seven are banks or owned by banks and just one is an independent company which means that the market is heavily dominated by the banks. Nearly 71% of factoring in 2015 comes from the domestic market, 27% comes from exports and 2% from import. The Postbank Bulgaria experts expect additional factoring market growth of 8% in 2016.

Considering actual factoring risks on the market, specific are the risk of trade cross-subsidizing, the bureaucracy risks of contract termination and binding with factor’s requirements, risk of company’s financial stability to be influenced by outside factors and third-part risk of damaging long-term trade relations between clients and suppliers [1]. More general is the risk of implicit increase of credit volume of the major banking institutions through factoring which is not effectively regulated at a macroeconomic level. At the same time the growth of that market is still limited by the legislation holes, grey economy, vague supply and weak understanding of the benefits of that service by a great part of the businesses.

References

- Raykov, E. (2016). “Specific risks of financing through factoring”, 12th International Scientific Conference of Young Scientists “The Economy of Bulgaria and European Union: Science and Business” (collection of papers), University of National and World Economy, Sofia, Bulgaria, 11 November 2016

- FCI Factoring Statistics. – Available at : https://fci.nl/en/about-factoring/statistics (date of appeal 9.12.2016.). – Title screen.

- Post Bank Statistics. – Available at : https://www.postbank.bg/bg-BG/AboutUs/04MediaCenter/.NewsDetail?id=ecbcae69-f40c-4d84-bff1-62612fd59f8a (date of appeal 9.12.2016.). – Title screen.

|